If you’re currently renting the space you live in, you may have had someone tell you that you’re wasting your money or throwing it away. In Phoenix, the owner-occupied housing rate is 56.1%. That means that over 40% of Phoenix residents rent. So you’re not alone in paying to live in an apartment, condominium, townhome, or single-family home. But are you really wasting your money?

Renting vs. owning

Whether you rent or own, you’re still spending money for a place to live. Renting is sometimes the best option for people who are new to a city. You might be starting a new job and want to get to know the area before you contemplate putting down permanent roots. With a rental, you typically know what your expenses will be for the coming year, although you may face an increase at the end of your leasing period. And when the year is up, you can move somewhere else. The downside is the building owner may sell the property unexpectedly or convert your building to condos.

The main thing you’re missing when renting is equity. If you rent for $2,000 a month, at the end of the year you will have spent $24,000. What do you have to show for it? Memories and receipts. If you had spent your money towards a mortgage payment, you would have increased your share of ownership, or your personal stake in your home. Over the years, renters remain at zero equity while homeowners continue to accrue a larger share of their property. Their home is not just a place to live — it becomes an asset — and homeowners can use that asset in several ways. They can tap into their equity for a loan, allow the equity to accrue over time as an investment, or convert the equity to cash when selling the home.

Are you interested in purchasing a home in the near future? If you want to make the leap from renter to homeowner, here are some things for you to consider.

The main thing you’re missing when renting is equity. If you rent for $2,000 a month, at the end of the year you will have spent $24,000. What do you have to show for it? Memories and receipts. If you had spent your money towards a mortgage payment, you would have increased your share of ownership, or your personal stake in your home. Over the years, renters remain at zero equity while homeowners continue to accrue a larger share of their property. Their home is not just a place to live — it becomes an asset — and homeowners can use that asset in several ways. They can tap into their equity for a loan, allow the equity to accrue over time as an investment, or convert the equity to cash when selling the home.

Are you interested in purchasing a home in the near future? If you want to make the leap from renter to homeowner, here are some things for you to consider.

Explore and dream

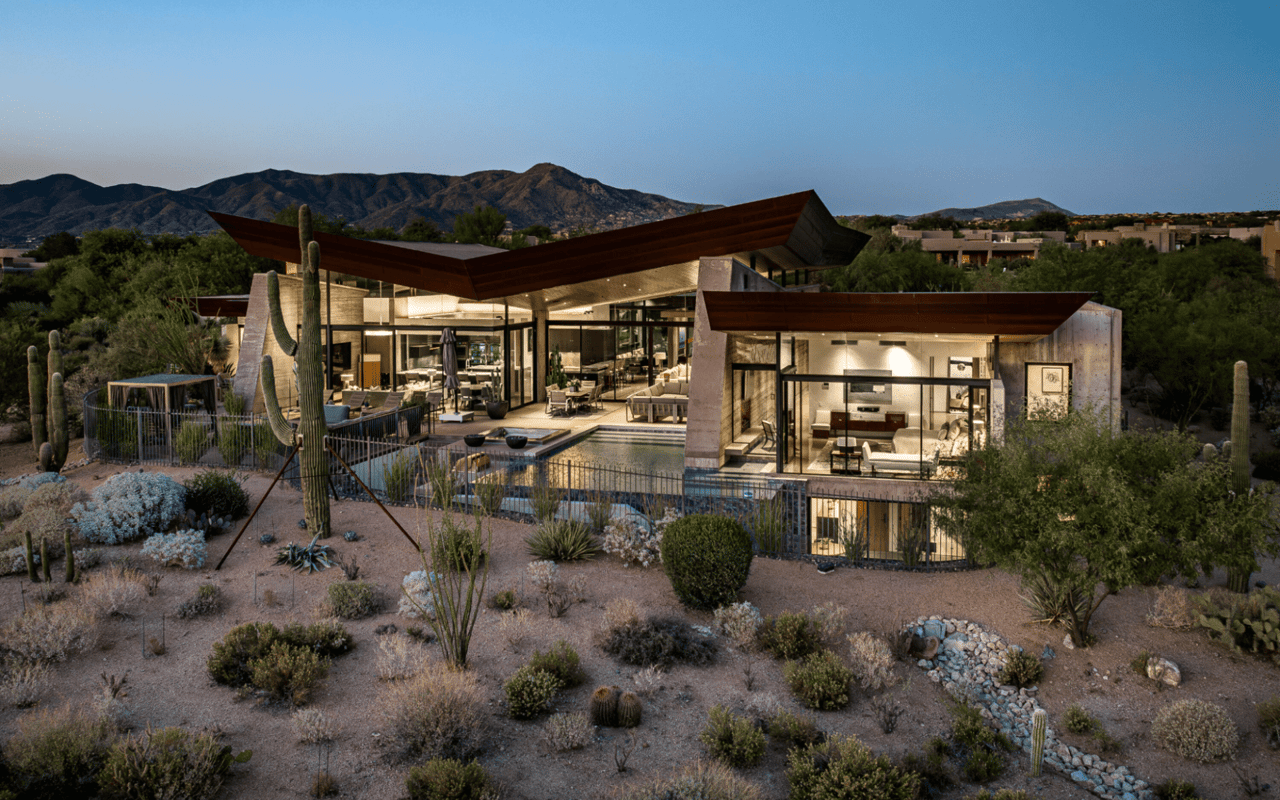

To make the move from renter to homeowner, you need to make goals that will motivate you to make life changes that will help facilitate a home purchase. Get online and search for homes. If you don’t like the area where you reside, look for better neighborhoods away from the congestion and close quarters of city life, such as North Scottsdale. A simple web search for new homes in North Scottsdale will reveal a beautiful range of architectural styles on spacious lots. Take a drive around different communities and look at homes for sale, as well as any community amenities and features. When you get that “I want to live there” feeling, take that dream and let it be your impetus as you plan for a future of homeownership.

Steady gets you ready

When you purchase a home, you need to employ leverage, not in the sense of effort, but in terms of borrowing power. A home is a major investment, and lenders want to be certain that you’re able to succeed in your financial commitment. They will look not just at your income but at the length of time that you have been with the same employer. In most cases, you’ll need to establish a continuous employment history of two years minimum. If you’ve just changed jobs, or are planning on changing jobs soon, consider how this will affect your mortgage application. Stay the course with that employer throughout your loan to demonstrate your stability. You may think you have the necessary income for a new home in North Scottsdale, but if you’ve only been with your company for six months, the financer may think differently.

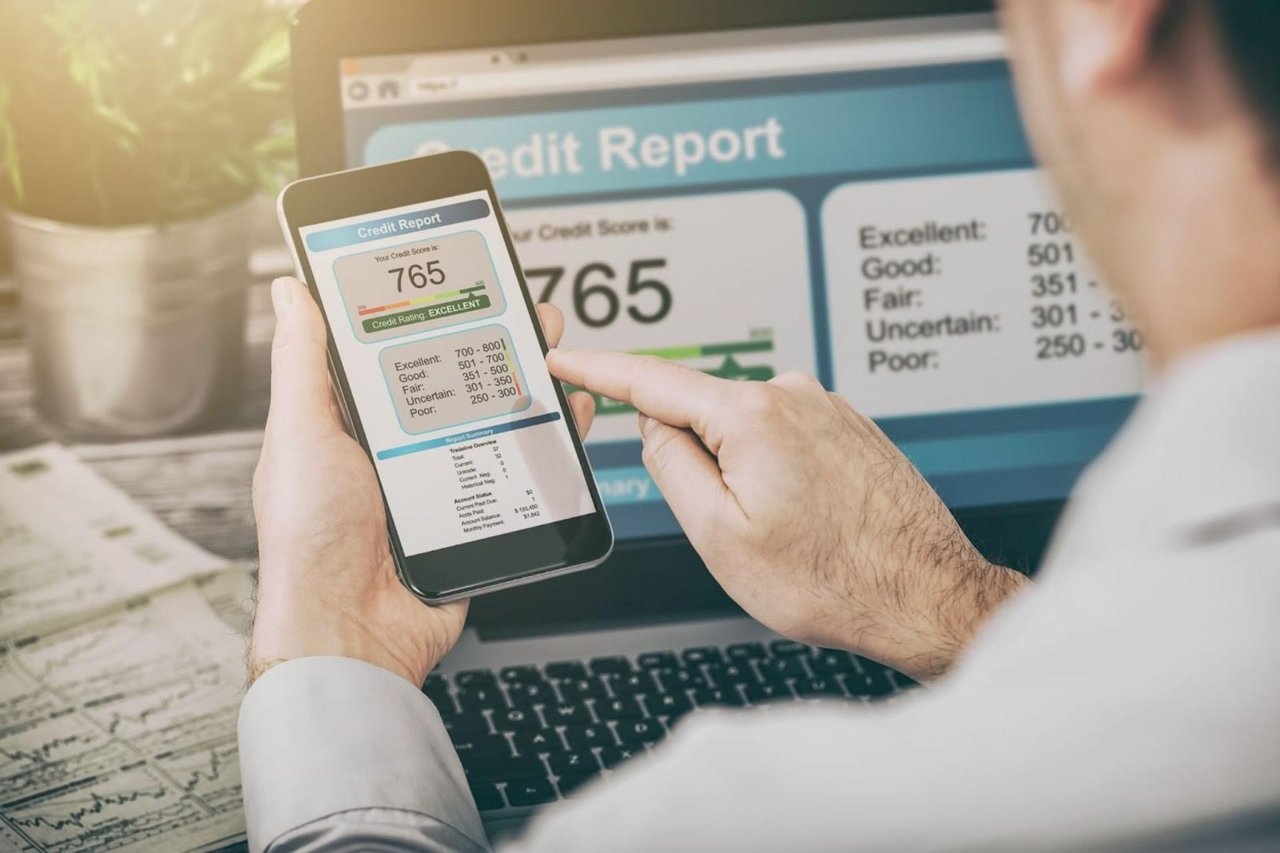

Establish good credit

When it’s time to apply for a mortgage, the higher your credit score, the better. Your credit score affects the ever-important interest rate that you’ll be paying, as well as the types of mortgages available to you. Credit bureaus calculate your credit score via a complicated algorithm that considers several factors, primarily your history of payments, your use of available credit, and your credit history over time. Paying your bills on time is perhaps the best way to build good credit. Also, take a look at your credit utilization. A common rule of thumb is to keep your debt load below 30% of your total available credit. Another important area to look at is how long your credit accounts have been open. Basically, you want them to be established, long-term accounts, not newly opened. One sure way to lower your credit score is to have several new accounts on your history.

If your credit score isn’t where it needs to be, make plans to increase your score and stick to them. Good credit is built over time, and internet ads or companies that promise to boost your score quickly may be selling something that cannot be delivered.

If your credit score isn’t where it needs to be, make plans to increase your score and stick to them. Good credit is built over time, and internet ads or companies that promise to boost your score quickly may be selling something that cannot be delivered.

Make saving a priority

Saving money for a down payment and closing costs is not easy, especially in a period of high inflation. In fact, high inflation can actually erode your savings. There is a common misconception that a 20% down payment is a requirement to buy a home. While this isn’t an actual requirement to obtain a mortgage, it does eliminate the additional cost of private mortgage insurance, or PMI. Mortgage lenders vary in their required down payments, but generally, they range from three to five percent. Closing costs, on average, are an additional two to five percent of the amount borrowed. If you don’t have a budget, take the time to make one. And then live within that budget. Saving money means hard choices, as you will have to set aside less important needs and desires for your primary goal of getting into a new home in North Scottsdale.

Get pre-approval

When you’ve got a steady job and income, have built your credit score, and have set aside enough money for a downpayment and closing costs, it’s time to get pre-approved for a mortgage. This step is different from pre-qualification, as it requires more documentation and has more stringent guidelines. Your lender will assess your borrowing capacity through the financial information you provide. They will supply you with a pre-approval letter, which states that they are willing to lend you up to a set amount of money. This is not a guaranteed offer for a loan. Instead, it provides you with a target figure so that you can establish a price range for the homes you are interested in.

Find a real estate agent

With your financial ducks in a row and your pre-approval letter in hand, it’s time to find a real estate agent. You want someone you can trust with a proven track record of sales, good recommendations, and thorough first-hand knowledge of the community you’re interested in. There are many agents to choose from, so do your research and interview a short list of agents.

If you’re looking for new homes in North Scottsdale, consider turning to the local experts at POWER+. With decades of experience that you can rely on, POWER+ team ranks consistently as high-quality professionals who provide unmatched client services. They can equip you with the customized assistance you need to make the leap from renter to homeowner, so be sure to contact them today to get started.

If you’re looking for new homes in North Scottsdale, consider turning to the local experts at POWER+. With decades of experience that you can rely on, POWER+ team ranks consistently as high-quality professionals who provide unmatched client services. They can equip you with the customized assistance you need to make the leap from renter to homeowner, so be sure to contact them today to get started.